Mobile banking transactions at a server with authentication

Patent No. US10235664 (titled "Mobile banking transactions at a server with authentication") on Mar 19, 2014. The application was issued on Mar 19, 2019.

What is this patent about?

'664 is related to the field of data communications and wireless devices, specifically addressing the increasing use of mobile communication devices for conducting payment transactions. The background acknowledges the growing trend of using cellular phones and PDAs for purchasing goods, paying bills, and transferring funds. The patent aims to improve the security and efficiency of these mobile payment processes.

The underlying idea behind '664 is to leverage a mobile device as a secure intermediary for online payment transactions initiated at a point-of-sale (POS) device. Instead of the POS directly communicating sensitive payment information to a payment entity, it routes the authorization request through the user's mobile device. This allows the mobile device to act as a secure vault, handling the sensitive data and communicating directly with the payment entity, thereby reducing the risk of data theft at the POS.

The claims of '664 focus on a method, system, and remote management server for processing a mobile banking transaction. The core of the claims involves receiving user identification and PIN information at a remote server from a non-browser-based application on a mobile device, authenticating the user, receiving a transaction request from the same application, processing the transaction, and sending a digital artifact back to the application for display. The mobile device is specified to have both cellular and Wi-Fi connectivity.

In practice, a user initiates a purchase at a POS, which then prompts the user to authorize the payment via their mobile device. The POS sends the transaction details to the user's mobile app. The app, after user authentication (e.g., PIN entry), securely transmits the payment authorization to a remote management server (e.g., a bank). The server processes the payment and sends a confirmation back to the app, which then relays the result to the POS to complete the transaction. A digital artifact, such as a receipt, is then sent to the mobile app.

This approach differs from traditional methods where the POS directly handles sensitive payment data. By using the mobile device as a secure intermediary, the patent aims to enhance security by ensuring that sensitive information is only transmitted between the user's device and the payment entity. Furthermore, the use of a non-browser-based application allows for a more controlled and secure environment compared to a standard web browser, potentially mitigating risks associated with browser-based vulnerabilities. The system also facilitates the delivery of digital artifacts directly to the user's mobile device, improving the overall transaction experience.

How does this patent fit in bigger picture?

Technical Landscape

In the late 2000s when ’664 was filed, mobile commerce was emerging at a time when financial transactions were typically implemented using dedicated web browsers or SMS-based messaging. Systems commonly relied on standard cellular data protocols for simple information exchange, but hardware and software constraints made the seamless integration of local non-browser applications with remote banking servers non-trivial. During this era, the coordination between a mobile device's local interface and a remote management server for real-time payment authorization often faced limitations in how security credentials and digital artifacts were synchronized across different wireless communication channels.

Prosecution Position

The examiner allowed the application because the prior art failed to disclose the specific combination of a remote management server receiving a user's identification code and PIN-related information directly from a non-browser application installed on a mobile device. Specifically, the hardware and software configuration allows the remote server to authenticate the user and process a mobile banking transaction based on data sent from this dedicated application, which then receives and displays a specific digital artifact on the mobile device's screen as a result of the transaction.

Claims

This patent contains 45 claims, with claims 1, 2, and 3 being independent. The independent claims focus on a method, system, and remote management server for processing mobile banking transactions using a non-browser based application on a mobile device. The dependent claims generally elaborate on and refine the elements and features described in the independent claims, providing more specific details and functionalities related to the mobile banking transaction process.

Key Claim Terms New

Definitions of key terms used in the patent claims.

Litigation Cases New

US Latest litigation cases involving this patent.

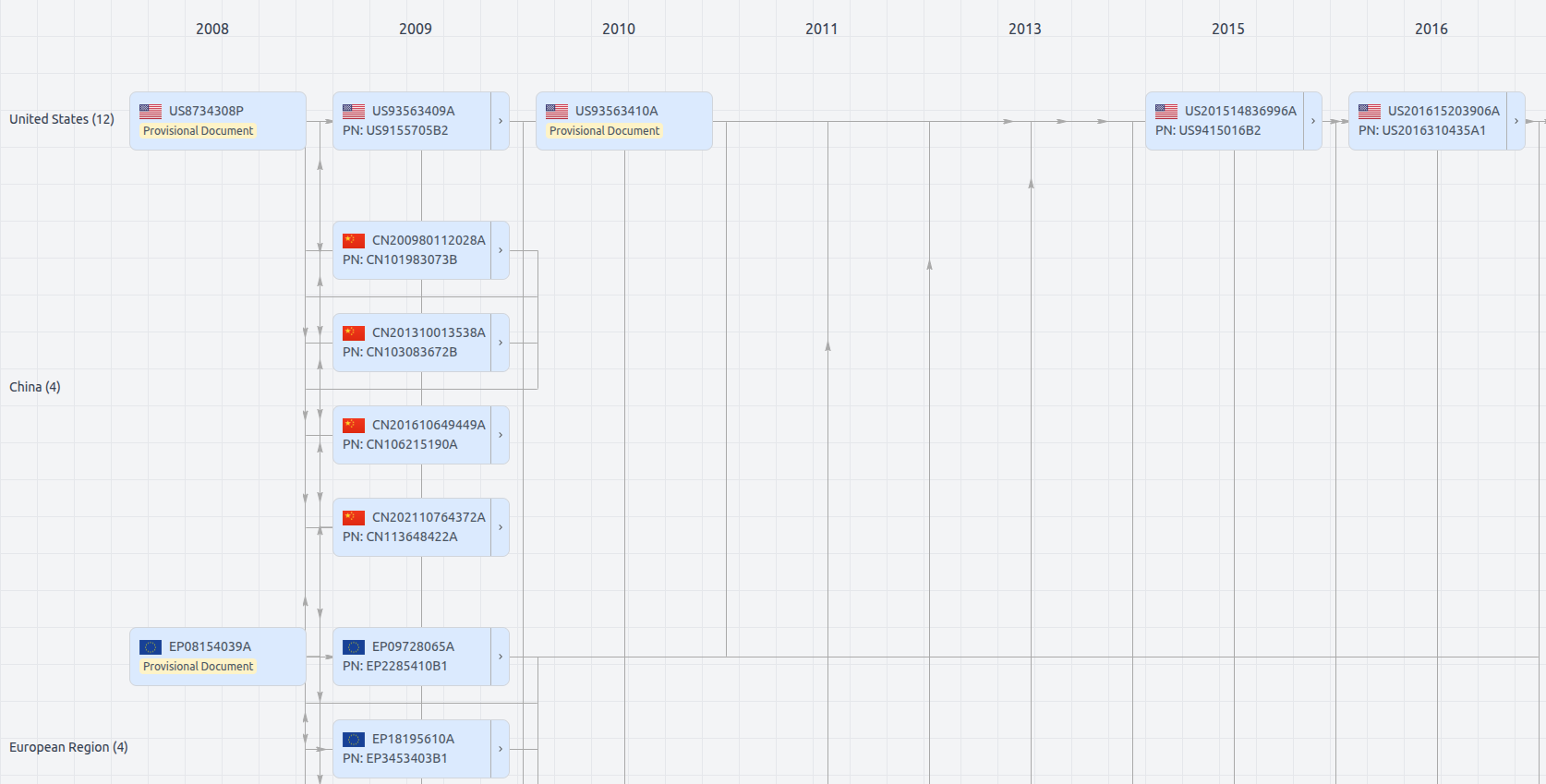

Patent Family

File Wrapper

The dossier documents provide a comprehensive record of the patent's prosecution history - including filings, correspondence, and decisions made by patent offices - and are crucial for understanding the patent's legal journey and any challenges it may have faced during examination.

Get instant alerts for new documents

US10235664

- Application Number

- US14219223A

- Filing Date

- Mar 19, 2014

- Publication Date

- Mar 19, 2019

- External Links

- Slate, USPTO , Google Patents