Mobile communication device near field communication (NFC) transactions

Patent No. US9378493 (titled "Mobile communication device near field communication (NFC) transactions") on Sep 14, 2012. The application was issued on Jun 28, 2016.

What is this patent about?

'493 is related to the field of mobile payment security, specifically addressing vulnerabilities associated with conducting transactions via mobile communication devices. The background acknowledges the increasing use of mobile devices for payment transactions and the critical need to protect users from fraud due to loss or theft of these devices. Existing solutions lacked robust security measures, leaving sensitive financial data at risk.

The underlying idea behind '493 is to implement a layered security approach for mobile payment transactions. This involves hosting the mobile payment application on a remote server, monitoring data transmission between the mobile device and the server, and employing various security measures such as session keys, remote locking, and payment limit PINs. The key insight is that by centralizing control and monitoring, the risk of data compromise is significantly reduced.

The claims of '493 focus on conducting a Near Field Communication (NFC) transaction using a mobile communication device. The device has a secure element with an application that uses the NFC protocol and an identification code. When an NFC terminal detects a signal, the application runs and sends the identification code to the terminal. The terminal then sends the code to a management server, which forwards it to a transaction server for processing the NFC transaction using a payment method linked to the identification code.

In practice, the invention works by leveraging a secure element within the mobile device to store sensitive payment information. When a user initiates an NFC transaction, the secure element application is activated, transmitting the necessary data to the NFC terminal. The management server monitors this transmission, ensuring that the session key is valid and that no unauthorized activity is occurring. If the transaction exceeds a pre-defined limit, the user is prompted for a PIN, adding an extra layer of security.

The differentiation from prior approaches lies in the combination of remote hosting, centralized monitoring, and multi-factor authentication. Unlike traditional mobile payment systems that store sensitive data directly on the device, '493 minimizes the amount of data stored locally, reducing the risk of data theft in case of device loss or compromise. The use of session keys and remote locking capabilities further enhances security by allowing for immediate disabling of the application in case of suspected fraud.

How does this patent fit in bigger picture?

Technical Landscape

In the mid-2000s when ’493 was filed, mobile commerce was emerging at a time when financial transactions were typically implemented using dedicated hardware terminals or desktop web browsers. When systems commonly relied on static credentials and basic cellular data protocols for remote banking, software constraints made the secure, real-time management of sensitive payment data on a handheld device non-trivial. During this era, the integration of mobile application hosting with centralized server-side monitoring was a developing architecture, as hardware limitations often restricted the complexity of security protocols that could be executed locally on a mobile processor.

Prosecution Position

The examiner allowed the application because the applicant’s amendments and supporting arguments, submitted on March 9, 2016, successfully distinguished the invention from previous technologies. Specifically, the examiner stated that the current version of the claims is not taught, suggested, or rendered obvious by any of the prior art references currently on record, whether those references are considered individually or in combination.

Claims

This patent contains 16 claims, with independent claims 1 and 9. Independent claim 1 focuses on a method for conducting an NFC transaction using an NEC protocol and a mobile communication device, while independent claim 9 focuses on a mobile device using an NFC protocol for an NFC transaction. The dependent claims generally elaborate on the method and mobile device by adding details such as biometric authentication, coupon application, and digital artifact delivery.

Key Claim Terms New

Definitions of key terms used in the patent claims.

Litigation Cases New

US Latest litigation cases involving this patent.

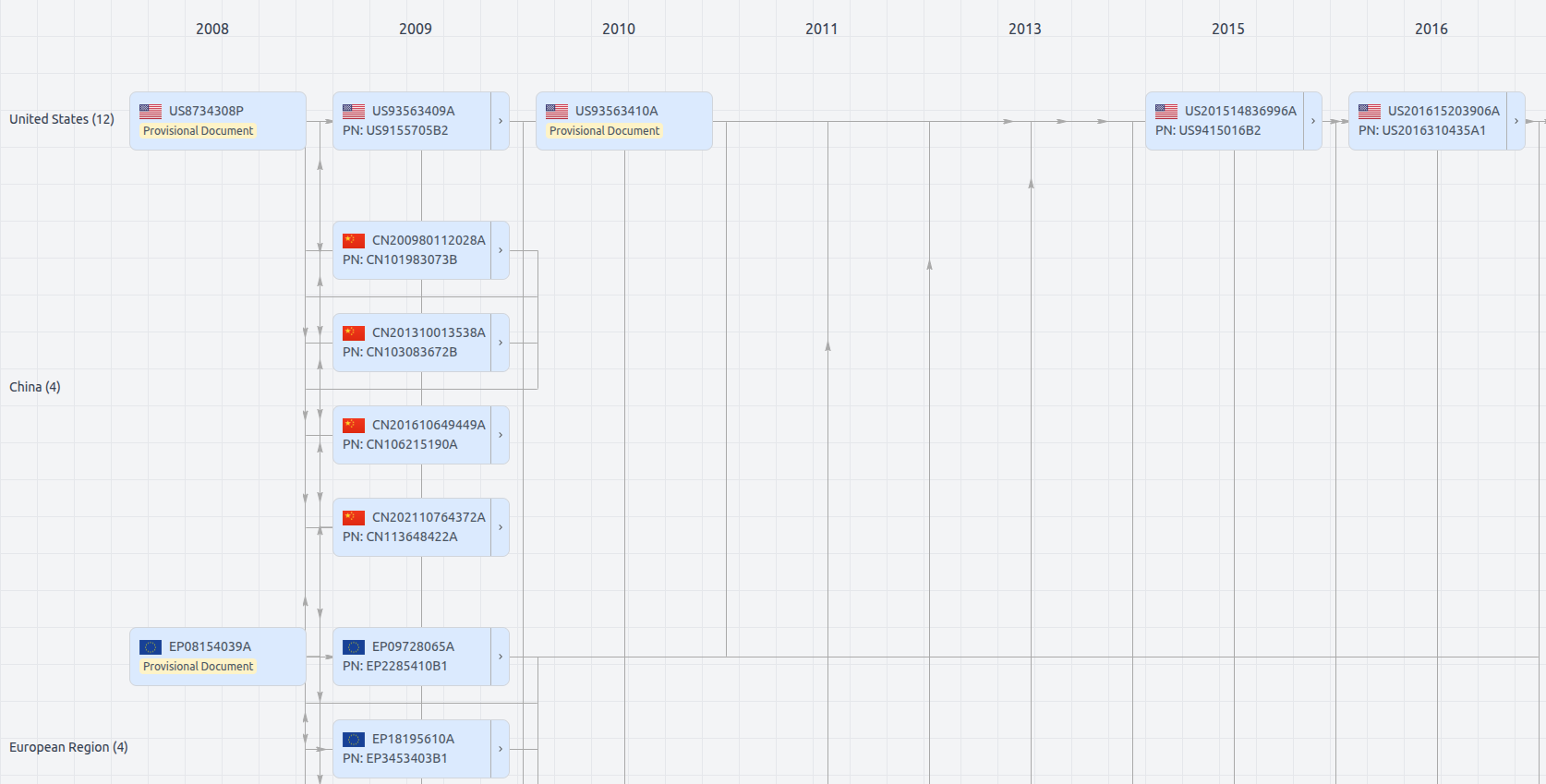

Patent Family

File Wrapper

The dossier documents provide a comprehensive record of the patent's prosecution history - including filings, correspondence, and decisions made by patent offices - and are crucial for understanding the patent's legal journey and any challenges it may have faced during examination.

Get instant alerts for new documents

US9378493

- Application Number

- US13620632A

- Filing Date

- Sep 14, 2012

- Publication Date

- Jun 28, 2016

- External Links

- Slate, USPTO , Google Patents